Institutional Insights: Deutsche Bank SP500 Flows & Positioning

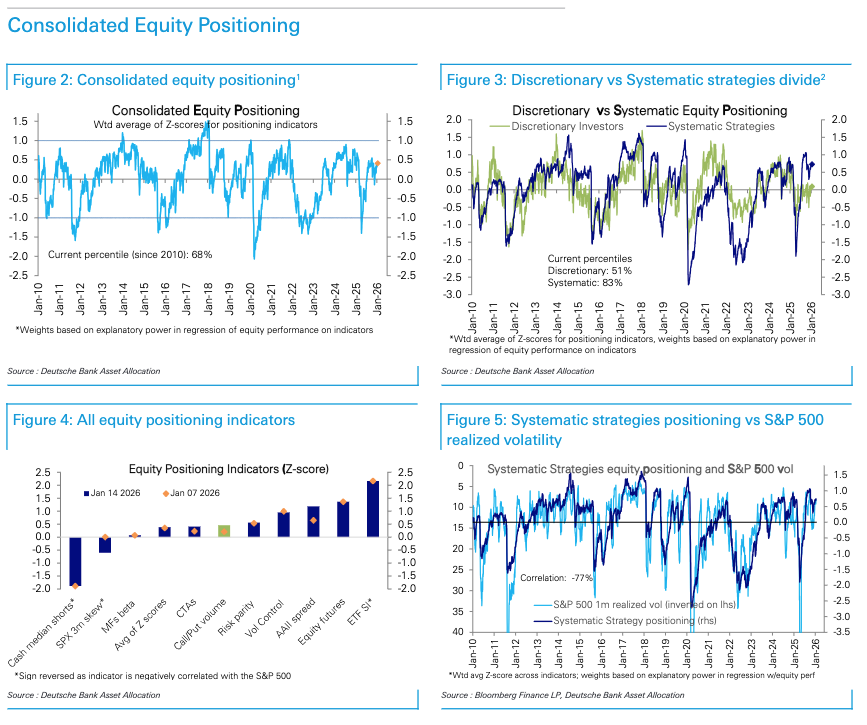

Positioning Trends Moving Higher: Aggregate equity positioning edged higher this week, maintaining a modestly overweight stance (0.41 standard deviations, 68th percentile). Discretionary investor positioning increased slightly to just above neutral, remaining near the upper boundary of the cautious range observed over the past ten months (0.13 standard deviations, 54th percentile). Systematic strategies also slightly raised their positioning (0.75 standard deviations, 84th percentile), staying overweight but not at extreme levels. While sentiment continued to improve, actual positioning remains slower to adjust.

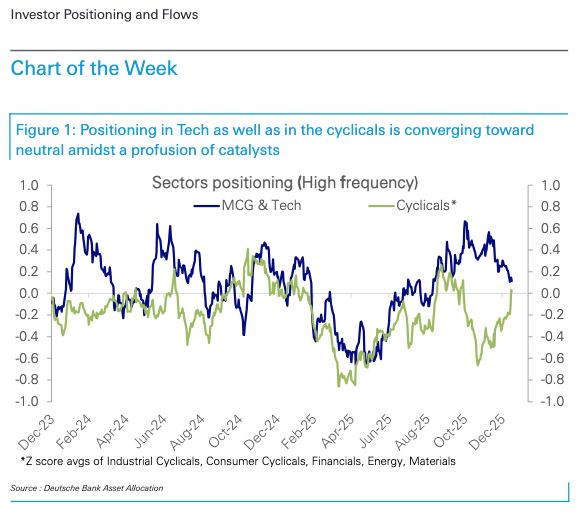

Sector Positioning Converging Toward Neutral: Across sectors, positioning is gravitating toward neutral amid a variety of catalysts. Tech sector positioning continued its gradual decline this week, dropping from a significant overweight in late October to nearly neutral levels. Conversely, cyclicals have shown the opposite trend, rising from a meaningful underweight to near-neutral positioning. Most sectors now hover within a tight range around neutral (approximately +/- 0.2 standard deviations), with the exceptions being Staples and Real Estate, which remain more underweight. Given the diverse mix of micro and macroeconomic, political, and geopolitical catalysts influencing stocks and sectors, the overall shift toward neutral positioning is unsurprising.

Equity Fund Inflows Rebound Significantly: Equity funds saw their second-largest weekly inflows on record, totaling $71.1 billion. Early-year inflows are typically strong, and this week’s activity was broad-based, led by the US ($36.5 billion), broad-global funds ($15.0 billion), and emerging markets ($16.8 billion), with China accounting for $8.5 billion of the EM inflows. Among sector-specific funds, Materials ($5.6 billion) and Industrials ($3.6 billion) experienced record inflows, while Tech ($5.4 billion), Financials ($3.3 billion), and Telecom ($1.6 billion) also saw robust inflows. Bond fund inflows also surged, reaching $23.4 billion.

Positioning and Flows Summary:

- Equity Positioning: Aggregate equity positioning modestly overweight (0.41sd, 68th percentile). Discretionary investors slightly above neutral (0.13sd, 54th percentile), near cautious range. Systematic strategies stayed overweight (0.75sd, 84th percentile).

- Discretionary Details: Call/put volume ratio rose (69th percentile), driven by ETF/index options; single stock options declined. Sectors: Materials, Energy, and defensives saw higher net call volumes; MCG & Tech, Consumer Cyclicals, and Financials declined. S&P 500 options skew rose to mid-range since Aug 2024. Most-shorted stocks marginally outperformed. Investor sentiment highest in 14 months, net bullish for seven weeks (79th percentile).

- Systematic Strategies: Vol control funds slightly reduced equity allocation (99th percentile), maintaining low sensitivity to selloffs. CTAs increased equity long positioning across regions, notably Europe (88th percentile) and EM (78th percentile). US bonds saw a sharp drop in long positioning, Europe and Japan increased shorts, while UK bonds edged higher. Commodities: Gold (57th percentile) and copper (80th percentile) long positions rose; oil short positions flat (11th percentile). Risk-parity funds’ equity allocation steady (79th percentile), with slight commodity allocation cuts.

- Sector Positioning: Cyclicals increased, Tech slightly trimmed. Energy (78th percentile) and Materials (71st percentile) modestly overweight. Real Estate (18th percentile) and Consumer Staples (9th percentile) sharply underweight.

- Weekly Fund Flows: Equity funds received $71.1bn, second-largest inflow on record, driven by US ($36.5bn) and EM ($16.8bn, led by China and South Korea). Materials ($5.6bn) and Industrials ($3.6bn) hit record highs; Tech ($5.4bn) rebounded after outflows. Bond funds inflows surged ($23.4bn), led by IG ($6.1bn), Government bonds ($3.4bn), and Munis ($2.9bn). Money market funds saw large outflows (-$62.1bn), driven by the US (-$70.9bn).

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!