Dollar On Watch: Iran War & US Inflation

Iran War Continues

The US Dollar is on watch this week as the war with Iran rages on and traders prepare for the latest US CPI data on Wednesday. A record push higher in oil prices which saw crude topping $120 p/b earlier today has raised fears over the impact on the global economy of a prolonged conflict. Elevated energy prices pose a serious threat to the world economy and create a difficult landscape for central banks to navigate. Indeed, we’re already seeing traders stripping back easing expectations for the Fed and BOE, with projections now turning in favour of tightening this year if energy prices remain at lofty levels, stocking inflationary pressures.

Crude Softens on IEA Chatter

For now, DXY has pulled back from the day’s highs, in line with the reversal lower in crude. This is likely linked to speculation that the IEA will release strategic oil reserves in a bid to quell rampant crude prices. The FT reported earlier today that G7 leaders are scheduled to meet later today to discuss such a move, to be executed via the IEA. The group last did this in response to the upside price shock in oil seen in 2022 when Russia invaded Ukraine. If a release is announced, and does help push crude lower, USD should continue to cool as well. The extent to which that reaction is seen will depend on the scale of the release and also how the situation in the Middle East develops. As such, near-term volatility risks remain high.

US CPI On Weds

Midweek, traders will turn their attention to the latest inflation data. While clearly backseat to the war, any upside surprise should reinforce the view that the Fed is unlikely to ease in coming months, offering some fresh support for USD.

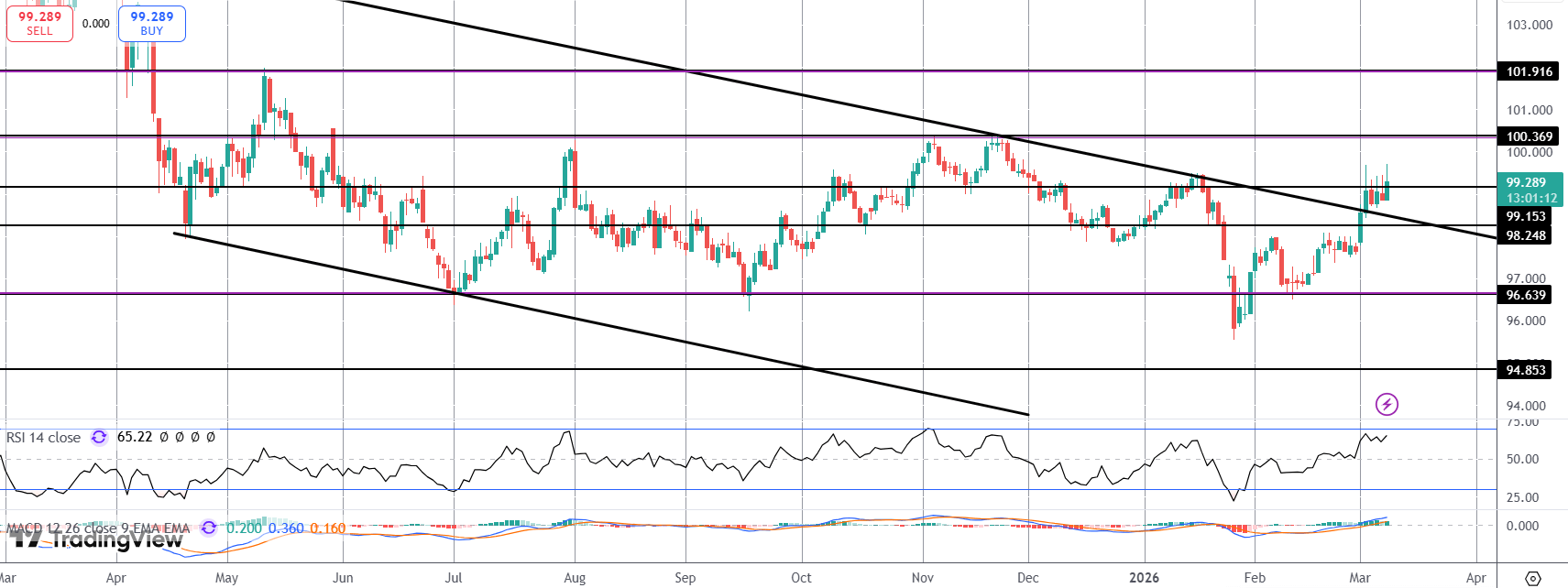

Technical Views

DXY

For now, the index remains caped around the $99.15 level following the breakout above the bear-channel highs. With momentum studies bullish, focus is on a fresh push higher with the $100-mark the next objective for bulls. Only a break back below the $98.24 level will shift the near-term bull view.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.